- You have no items in your shopping cart

- Continue Shopping

Content

- Five keys to understanding BBVA income statement

- Financial stability 10 years after the crisis

- Loans and Advances in Bank’s Balance Sheet

- Lie #1: The majority of assets on a bank’s balance sheet are not reported at fair market value

- Set a value for intangible assets

- Equity / capital

- Definition of Banks Balance Sheet

Exactly how the equity is made up will vary from company to company, depending on the business type and stage. To complete your balance sheet template you’ll need to add in details about the debts and liabilities your company owes. The Great Recession has also underscored the fact that banks held many asset-backed securities as well. United States banks are not permitted to own stocks, because of their risk, but, ironically, they can hold much riskier securities called derivatives.

It’s a Preferred Stock Dividend and it’s going to affect Net Income and get us Net Income to Common, but it should not be in this calculation for now. Now, on the Liabilities & Equity side we can do pretty much the same and take the Beginning Balance times the Interest Rate in each case, copy this down, and then do the same thing for Preferred Stock down here and so we have that. And then since we’re at the bottom we might as well just sum up everything above to make sure our numbers https://www.bookstime.com/articles/financial-statements-for-banks are adding up. So let’s take what we have here, the old number, the loan additions, and then we can factor in the Net Charge-Offs right here. And then for the Allowance for Loan Losses, let’s go over here and just link to our Ending Reserve Balance right there, so we have that. The Annual Reserve Balance is just the beginning balance plus these Net Charge-Offs really minus the charge-offs and plus the recoveries, and then we add our Provisions right here, so get to $12.

Five keys to understanding BBVA income statement

A bank has assets such as cash held in its vaults and monies that the bank holds at the Federal Reserve bank (called “reserves”), loans that are made to customers, and bonds. Moving on, we can contrast the balance sheet of U.S. households with that of nonfinancial firms and depository banks. Starting with the first, we combine corporate and noncorporate balance sheets to obtain the information in the following table.

Changes in Deposits, this is considered an operational item for a lot of banks, so we take our Ending Balance and then subtract our Beginning Balance right here. So as a starting point we’re always going to use Net Income to Common in most of our models anyway on the site. Even when companies in other countries present their Cash Flow Statements differently and you use the direct method, or start with pre-tax income, we generally think it’s easiest and best to start with net-income. So this is what the diagram looks like at a high level; the difference is that in this lesson we’re going to move into it at a much lower level. We have a bank’s Balance Sheet with the Assets side right here, with Liabilities & Equity right below it, and then Regulatory Capital below that.

Financial stability 10 years after the crisis

The successful launch of the new product would require a near-immediate start for the 45- to 60-day construction and preparation period. We return to these issues when considering emerging market financial crises in Section 8. At the end of the first period, and subsequently, all components of owners’ equity are restated by applying a general price index from the start of the period to date of contribution and https://www.bookstime.com/ any movements disclosed as per IAS 1. Where fixed assets are impaired they must be reduced to their recoverable amount and inventories to NRV. If a general price index is not available then an estimate should be based on movements in the exchange rate between the functional and a relatively stable foreign currency. Table 7 provides information on the assets that serve as collateral for Federal Reserve notes.

So for Return on Common Equity, we want Net Income to Common here because we’re leaving out preferred stockholders. And then we can divide by the average Common Stockholders’ Equity. Now for Changes in Other Securities, let’s go and get our Beginning Balance and subtract our Ending Balance. We’re on the Assets side so if this increases we want it to be a negative. And then Changes in Other Assets, go over here and then subtract the ending one.

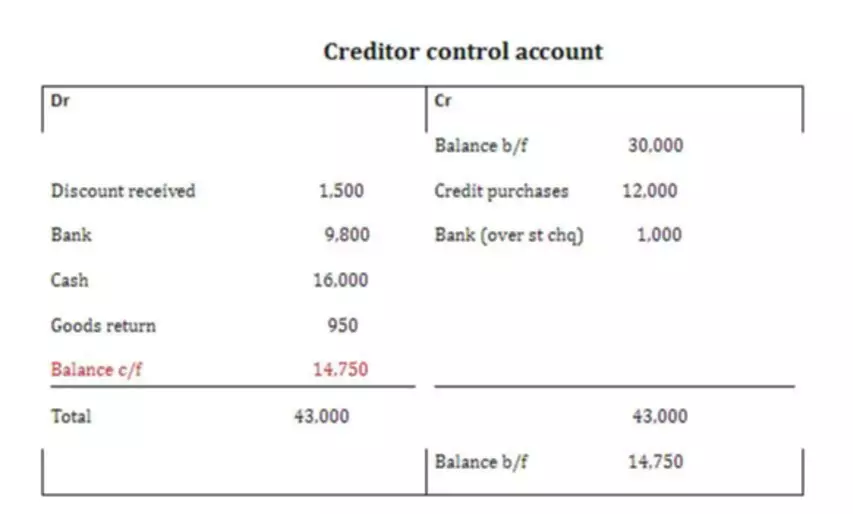

Loans and Advances in Bank’s Balance Sheet

Once you list all your assets and their value, you can calculate your total assets by adding your current assets, noncurrent assets and intellectual properties. For noncurrent assets in particular, you should be prepared to explain how you determined their fair value. You can first list your current assets (cash, marketable securities or inventory), ordering the ones your company can quickly turn into cash before the others. The assets on your balance sheet should always balance with the total of your company’s liabilities plus equity. Long-term liabilities are obligations that will not be paid off in the coming year.

- Initially, the investor has total assets of $200, a loan of $100 and net worth of $100.

- Instead what I’m going to do is just keep all of these items constant for now.

- Larger banks tend to be on the low end of that range (50-75%) while smaller banks tend to be on the high end of that range (75-95%).

- As a last resort banks can also borrow from the Federal Reserve (Fed), though they rarely do this since it indicates that they are under financial stress and unable to get funding elsewhere.

As the collateral can take either forms, arbitrage CDOs can be either CLOs or collateralised bond obligations (CBOs). Market practitioners often refer to all arbitrage deals as CDOs for simplicity, irrespective of the collateral backing them. The key motivation behind arbitrage CDOs is, unsurprisingly, the opportunity for arbitrage, or the difference between investment grade funding rates and high-yield investment rates.

Lie #1: The majority of assets on a bank’s balance sheet are not reported at fair market value

In contrast, the second tells us about the flow of revenue and expenditure, providing information about current income net of payments, or profitability. These two accounting statements are closely linked, as net income or profit will accumulate on the balance sheet, adding to (or subtracting from) assets and net worth. The exact impact of these activities on a bank’s balance sheet can be difficult to quantify, but the investor who is determined to extract alpha from bank stocks should at least make the attempt. In my opinion, the most interesting of these OBS activities are contingent liabilities such as pending lawsuits, indemnity agreements, and other guarantees.

What is on a bank’s balance sheet?

In short, a bank's balance sheet is a record of everything it owns, is owed, or owes. The balance sheet comprises three distinct parts: assets, liabilities and shareholder equity.

Equity capital gets depleted when banks take losses, and when it gets to be too low, banks have to raise more capital from shareholders. Silicon Valley Bank tried to do this, and when potential investors said no, it helped precipitate the collapse of the bank. For example, the Fed’s liquidity support operations for primary dealers and money market mutual funds clearly fit in this category. Many banks make mortgage loans so that people can buy a home, but then do not keep the loans on their books as an asset. These loans are often “securitized,” which means that they are bundled together into a financial security that is sold to investors.